| ← Back to Inputs & Pricing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

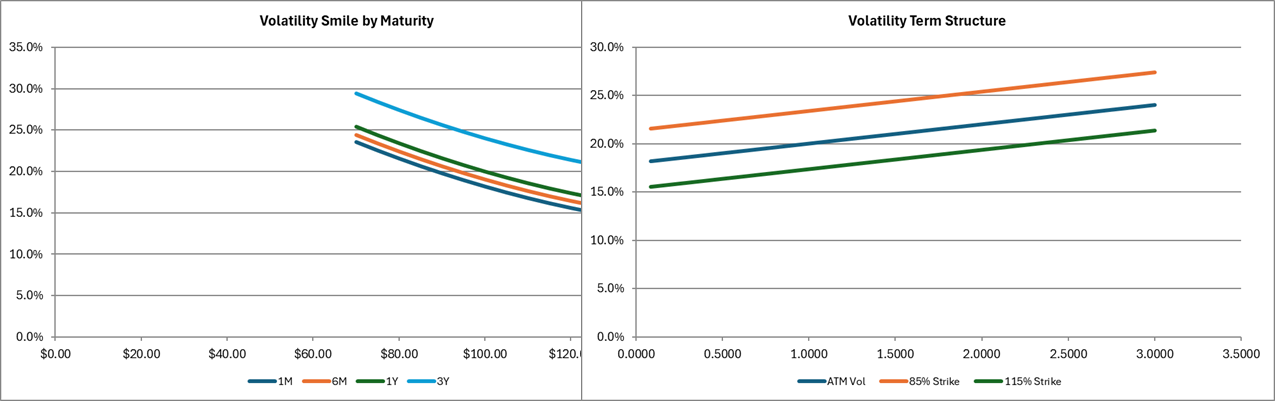

VOLATILITY SURFACE |

|

|

|

|

|

Implied Volatility by Strike & Maturity (Sample

Skew Surface) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SURFACE PARAMETERS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ATM Volatility |

20.00% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Skew Parameter |

-0.15 |

(slope per 10% OTM) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Convexity Parameter |

0.10 |

(smile curvature) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Term Structure Slope |

0.02 |

(vol increase per year) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reference Strike |

$100.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

IMPLIED

VOLATILITY SURFACE (Strike vs Time to Expiration) |

|

|

|

|

|

Strike / Maturity |

1M |

2M |

3M |

4M |

6M |

9M |

1Y |

1.25Y |

1.5Y |

1.75Y |

2Y |

3Y |

|

|

|

|

|

(years) |

0.0833 |

0.1667 |

0.2500 |

0.3333 |

0.5000 |

0.7500 |

1.0000 |

1.2500 |

1.5000 |

1.7500 |

2.0000 |

3.0000 |

|

|

|

|

|

$70.00 |

23.6% |

23.7% |

23.9% |

24.1% |

24.4% |

24.9% |

25.4% |

25.9% |

26.4% |

26.9% |

27.4% |

29.4% |

|

|

|

|

|

$75.00 |

22.5% |

22.7% |

22.9% |

23.0% |

23.4% |

23.9% |

24.4% |

24.9% |

25.4% |

25.9% |

26.4% |

28.4% |

|

|

|

|

|

$80.00 |

21.6% |

21.7% |

21.9% |

22.1% |

22.4% |

22.9% |

23.4% |

23.9% |

24.4% |

24.9% |

25.4% |

27.4% |

|

|

|

|

|

$85.00 |

20.6% |

20.8% |

21.0% |

21.1% |

21.5% |

22.0% |

22.5% |

23.0% |

23.5% |

24.0% |

24.5% |

26.5% |

|

|

|

|

|

$90.00 |

19.8% |

19.9% |

20.1% |

20.3% |

20.6% |

21.1% |

21.6% |

22.1% |

22.6% |

23.1% |

23.6% |

25.6% |

|

|

|

|

|

$95.00 |

18.9% |

19.1% |

19.3% |

19.4% |

19.8% |

20.3% |

20.8% |

21.3% |

21.8% |

22.3% |

22.8% |

24.8% |

|

|

|

|

|

$100.00 |

18.2% |

18.3% |

18.5% |

18.7% |

19.0% |

19.5% |

20.0% |

20.5% |

21.0% |

21.5% |

22.0% |

24.0% |

|

|

|

|

|

$105.00 |

17.4% |

17.6% |

17.8% |

17.9% |

18.3% |

18.8% |

19.3% |

19.8% |

20.3% |

20.8% |

21.3% |

23.3% |

|

|

|

|

|

$110.00 |

16.8% |

16.9% |

17.1% |

17.3% |

17.6% |

18.1% |

18.6% |

19.1% |

19.6% |

20.1% |

20.6% |

22.6% |

|

|

|

|

|

$115.00 |

16.1% |

16.3% |

16.5% |

16.6% |

17.0% |

17.5% |

18.0% |

18.5% |

19.0% |

19.5% |

20.0% |

22.0% |

|

|

|

|

|

$120.00 |

15.6% |

15.7% |

15.9% |

16.1% |

16.4% |

16.9% |

17.4% |

17.9% |

18.4% |

18.9% |

19.4% |

21.4% |

|

|

|

|

|

$125.00 |

15.0% |

15.2% |

15.4% |

15.5% |

15.9% |

16.4% |

16.9% |

17.4% |

17.9% |

18.4% |

18.9% |

20.9% |

|

|

|

|

|

$130.00 |

14.6% |

14.7% |

14.9% |

15.1% |

15.4% |

15.9% |

16.4% |

16.9% |

17.4% |

17.9% |

18.4% |

20.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CALL OPTION

PRICES (Black-Scholes with Surface Volatility) |

|

|

|

|

|

Strike / Maturity |

1M |

2M |

3M |

4M |

6M |

9M |

1Y |

1.25Y |

1.5Y |

1.75Y |

2Y |

3Y |

|

|

|

|

|

$70.00 |

$30.12 |

$30.25 |

$30.37 |

$30.51 |

$30.81 |

$31.36 |

$32.00 |

$32.69 |

$33.41 |

$34.15 |

$34.89 |

$37.86 |

|

|

|

|

|

$75.00 |

$25.15 |

$25.29 |

$25.45 |

$25.62 |

$26.04 |

$26.78 |

$27.59 |

$28.44 |

$29.31 |

$30.17 |

$31.04 |

$34.41 |

|

|

|

|

|

$80.00 |

$20.17 |

$20.34 |

$20.56 |

$20.81 |

$21.38 |

$22.35 |

$23.35 |

$24.36 |

$25.37 |

$26.36 |

$27.33 |

$31.07 |

|

|

|

|

|

$85.00 |

$15.19 |

$15.44 |

$15.77 |

$16.14 |

$16.92 |

$18.14 |

$19.33 |

$20.50 |

$21.63 |

$22.73 |

$23.81 |

$27.87 |

|

|

|

|

|

$90.00 |

$10.27 |

$10.72 |

$11.24 |

$11.76 |

$12.78 |

$14.23 |

$15.59 |

$16.89 |

$18.13 |

$19.32 |

$20.48 |

$24.82 |

|

|

|

|

|

$95.00 |

$5.68 |

$6.50 |

$7.23 |

$7.89 |

$9.10 |

$10.73 |

$12.21 |

$13.59 |

$14.91 |

$16.17 |

$17.39 |

$21.94 |

|

|

|

|

|

$100.00 |

$2.21 |

$3.22 |

$4.04 |

$4.76 |

$6.03 |

$7.71 |

$9.23 |

$10.65 |

$11.99 |

$13.29 |

$14.54 |

$19.23 |

|

|

|

|

|

$105.00 |

$0.50 |

$1.22 |

$1.89 |

$2.51 |

$3.66 |

$5.24 |

$6.70 |

$8.09 |

$9.42 |

$10.71 |

$11.97 |

$16.72 |

|

|

|

|

|

$110.00 |

$0.05 |

$0.32 |

$0.70 |

$1.12 |

$2.01 |

$3.34 |

$4.66 |

$5.95 |

$7.21 |

$8.46 |

$9.68 |

$14.40 |

|

|

|

|

|

$115.00 |

$0.00 |

$0.06 |

$0.20 |

$0.42 |

$0.98 |

$1.98 |

$3.08 |

$4.21 |

$5.37 |

$6.53 |

$7.69 |

$12.30 |

|

|

|

|

|

$120.00 |

$0.00 |

$0.01 |

$0.04 |

$0.12 |

$0.42 |

$1.09 |

$1.93 |

$2.87 |

$3.88 |

$4.92 |

$6.00 |

$10.40 |

|

|

|

|

|

$125.00 |

$0.00 |

$0.00 |

$0.01 |

$0.03 |

$0.15 |

$0.55 |

$1.14 |

$1.88 |

$2.72 |

$3.62 |

$4.59 |

$8.72 |

|

|

|

|

|

$130.00 |

$0.00 |

$0.00 |

$0.00 |

$0.01 |

$0.05 |

$0.25 |

$0.64 |

$1.18 |

$1.84 |

$2.60 |

$3.44 |

$7.25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PUT OPTION

PRICES (Black-Scholes with Surface Volatility) |

|

|

|

|

|

Strike / Maturity |

1M |

2M |

3M |

4M |

6M |

9M |

1Y |

1.25Y |

1.5Y |

1.75Y |

2Y |

3Y |

|

|

|

|

|

$70.00 |

$0.00 |

$0.00 |

$0.00 |

$0.01 |

$0.08 |

$0.28 |

$0.57 |

$0.92 |

$1.31 |

$1.72 |

$2.15 |

$3.94 |

|

|

|

|

|

$75.00 |

$0.00 |

$0.00 |

$0.02 |

$0.05 |

$0.19 |

$0.51 |

$0.92 |

$1.37 |

$1.84 |

$2.33 |

$2.82 |

$4.78 |

|

|

|

|

|

$80.00 |

$0.00 |

$0.01 |

$0.06 |

$0.15 |

$0.40 |

$0.89 |

$1.43 |

$1.99 |

$2.54 |

$3.10 |

$3.64 |

$5.75 |

|

|

|

|

|

$85.00 |

$0.00 |

$0.07 |

$0.21 |

$0.40 |

$0.82 |

$1.50 |

$2.17 |

$2.82 |

$3.44 |

$4.05 |

$4.64 |

$6.86 |

|

|

|

|

|

$90.00 |

$0.06 |

$0.31 |

$0.62 |

$0.94 |

$1.56 |

$2.41 |

$3.18 |

$3.90 |

$4.58 |

$5.22 |

$5.84 |

$8.11 |

|

|

|

|

|

$95.00 |

$0.46 |

$1.04 |

$1.54 |

$1.99 |

$2.75 |

$3.72 |

$4.55 |

$5.30 |

$6.00 |

$6.65 |

$7.27 |

$9.53 |

|

|

|

|

|

$100.00 |

$1.96 |

$2.73 |

$3.30 |

$3.77 |

$4.56 |

$5.52 |

$6.33 |

$7.06 |

$7.72 |

$8.35 |

$8.95 |

$11.13 |

|

|

|

|

|

$105.00 |

$5.23 |

$5.68 |

$6.08 |

$6.44 |

$7.07 |

$7.86 |

$8.56 |

$9.20 |

$9.79 |

$10.36 |

$10.90 |

$12.92 |

|

|

|

|

|

$110.00 |

$9.76 |

$9.74 |

$9.84 |

$9.97 |

$10.29 |

$10.78 |

$11.27 |

$11.75 |

$12.22 |

$12.68 |

$13.14 |

$14.90 |

|

|

|

|

|

$115.00 |

$14.69 |

$14.43 |

$14.27 |

$14.18 |

$14.13 |

$14.24 |

$14.45 |

$14.72 |

$15.01 |

$15.33 |

$15.67 |

$17.10 |

|

|

|

|

|

$120.00 |

$19.67 |

$19.34 |

$19.05 |

$18.80 |

$18.45 |

$18.16 |

$18.06 |

$18.07 |

$18.16 |

$18.31 |

$18.50 |

$19.51 |

|

|

|

|

|

$125.00 |

$24.65 |

$24.30 |

$23.95 |

$23.63 |

$23.06 |

$22.44 |

$22.02 |

$21.77 |

$21.64 |

$21.59 |

$21.61 |

$22.14 |

|

|

|

|

|

$130.00 |

$29.63 |

$29.25 |

$28.88 |

$28.52 |

$27.83 |

$26.96 |

$26.28 |

$25.77 |

$25.40 |

$25.15 |

$24.99 |

$24.97 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Notes |

|

|

|

|

|

1. The volatility surface is generated using a

parametric model: Vol = ATM_vol + Skew*(moneyness) + Convexity*(moneyness^2)

+ Term_slope*(T-1). |

|

|

|

|

|

2. Blue input values can be adjusted to model

different surface shapes. Negative skew creates typical equity-like skew. |

|

|

|

|

|

3. Option prices in the surface grids use the

corresponding implied volatility from the surface (not the flat vol from

inputs). |

|

|

|

|

|

4. This is sample/illustrative data. In practice,

implied volatilities would be calibrated from market option prices. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|